简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

【MACRO Insight】Panoramic Analysis of US Non-Farm Data in June: Employment Resilience and Market Ripp

Zusammenfassung:1. Overall picture of data: unexpected growth and structural characteristics coexistIn June, non-farm payrolls increased by 147,000, which was higher than the expected 110,000 and the previous value w

1. Overall picture of data: unexpected growth and structural characteristics coexist

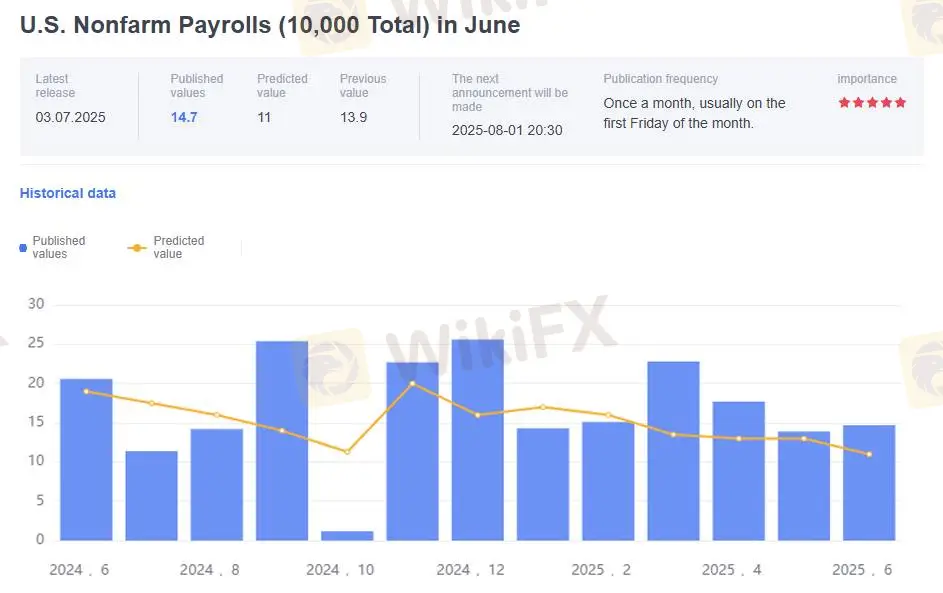

In June, non-farm payrolls increased by 147,000, which was higher than the expected 110,000 and the previous value was revised up from 139,000 to 144,000, exceeding economists' forecasts for the fourth consecutive time. The unemployment rate unexpectedly fell to 4.1%, lower than the expected 4.3% and the previous value of 4.2%, and has remained stable in a narrow range of 4.0%-4.2% since May 2024.

Wage growth showed a mild slowdown: the average hourly wage rose by 0.2% on a monthly basis, lower than the expected 0.3% and the previous value of 0.4%; the annual rate increased by 3.7%, slightly lower than the expected 3.9% and the revised previous value of 3.8%. This combination of "strong employment and slow wages" not only shows that the labor market is still vibrant, but also eases concerns about inflation rebound.

From the survey details, the household survey data revealed a deeper structure: the number of long-term unemployed increased by 190,000 to 1.6 million, accounting for 23.3% of the total number of unemployed; the labor force participation rate remained stable at 62.3%, and the employment-population ratio remained at 59.7%.

2. Market chain reaction: sudden changes in asset prices and policy expectations

After the data was released, financial markets quickly adjusted pricing: the U.S. dollar index rose in the short term, up 0.47% on the day to close at 97.308, hitting the 97 mark; spot gold fell by $19 in the short term, breaking below $3,320/ounce, and closed down 0.65% to $3,328.04/ounce.

Bets on the Fed's policies have reversed significantly: interest rate futures traders have completely abandoned their expectations of a rate cut in July, and the probability of a rate cut in September has dropped sharply from 98% before the data was released to 80%. However, the overnight index swap market still shows that the probability of a rate cut before September is over 70%, and there may be another rate cut before the end of the year, reflecting that the market's long-term expectations for policy easing have not been fundamentally shaken.

III. Employment structure: government-led growth and differentiation of the private sector

Institutional survey data showed that employment growth in June showed the characteristics of "strong government and weak private sector". The government sector added 73,000 jobs, of which state government education contributed 40,000 and local government education added 23,000. However, the federal government laid off 7,000 people for the fifth consecutive month, with a total of 69,000 layoffs since January.

The performance of the private sector was differentiated: the healthcare industry added 39,000 jobs, close to the average level in the past 12 months; the social assistance industry increased by 19,000 jobs, mainly from personal and family services; the construction industry bucked the trend and added 15,000 jobs, the largest increase since December last year, despite high mortgage rates and a weak real estate market in the spring.

IV. Interpretations from all parties: The debate over labor market resilience and policy paths

Nick Timiraos, the "Fed's mouthpiece," pointed out that the report showed that the labor market's "slow hiring, slow firing" characteristics continued. Jack McIntyre of Brandywine Global Investments believes that the strength of hard data (such as non-farm payrolls) proves that the Fed is right to stay on the sidelines, and market changes are flattening the yield curve, and the steepening of the curve may continue to close positions. Analyst Chris Anstey stressed that this report does not constitute an urgent reason for the Fed to cut interest rates immediately.

However, the decline in unemployment may be related to immigration policy: the number of foreign-born workers fell to 32.6 million in June, down 1.1 million from March, and fell for three consecutive months. Analyst Jonnelle Marte believes that the shrinking immigrant labor force may suppress unemployment and is related to the strengthening of border control. Jeffrey Rosenberg of BlackRock, the world's largest bond fund, is cautious, believing that the growth that relies on state and local government recruitment is actually weaker than expected, and the weakness of the private sector cannot be ignored.

5. U.S. Treasury Bonds and Policy Outlook: Goldman Sachs lowers its yield forecast

In summary, the June non-farm report not only shows the resilience of the US labor market, but also exposes structural contradictions. For the Federal Reserve, the combination of "robust employment + moderate wages" provides room for policy wait-and-see; for the market, in the game between hard data and soft expectations, short-term fluctuations and long-term trends, future trends will rely more on the further evolution of inflation data and fiscal policies.

Haftungsausschluss:

Die Ansichten in diesem Artikel stellen nur die persönlichen Ansichten des Autors dar und stellen keine Anlageberatung der Plattform dar. Diese Plattform übernimmt keine Garantie für die Richtigkeit, Vollständigkeit und Aktualität der Artikelinformationen und haftet auch nicht für Verluste, die durch die Nutzung oder das Vertrauen der Artikelinformationen verursacht werden.

WikiFX-Broker

Aktuelle Nachrichten

Türkei verzeichnet niedrigste Inflation seit dreieinhalb Jahren – doch die Zentralbank warnt

WikiFX

WikiFXInvestor Fabian Westerheide: Kann KI auch VC? Ja, aber.

WikiFXSchon als Kind mit 10 Euro vom Staat fürs Alter sparen: Was hinter dem Plan der Frühstart-Rente steckt

WikiFXWechselkursberechnung